Improving Insurance Underwriting: Behavioral Patterns and Actuarial Tables

Published on: 2024-08-10 18:38:12

Insurance Underwriting with Behavioral Data and Actuarial Insight

Insurance underwriting is changing. By combining behavioral pattern analysis with traditional actuarial methods, insurers can produce more accurate risk assessments and set policy pricing with more precision. This article explains how rule engines support that shift by enabling a more detailed evaluation of individual risk.

Shifting Gears in Insurance Underwriting

Insurance underwriting no longer relies only on demographic data and static actuarial tables. Insurers now use data analytics to add behavioral insight to their models. This shift supports a deeper view of individual risk, moving beyond broad demographic groups to more tailored risk assessments.

Understanding Behavioral Pattern Recognition

Behavioral pattern recognition examines individual behavior and lifestyle choices to identify risk factors more precisely. This approach works well when combined with rule engines that can process and evaluate complex datasets.

Implementing Rule Engines in Underwriting

Integrating Behavioral Data:

- Data Collection: Collect detailed data from telematics in auto insurance, such as average speed, frequency of hard braking, and driving times, as well as data from health trackers in life insurance, such as daily step count and heart rate variability.

- Rule Engine Configuration: Configure rule engines to analyze this data and identify risk patterns. Below are examples of specific rules:

- Rule 1: Auto Insurance Speeding Pattern: "If average driving speed > speed limit by 20% on more than 50% of trips, then increase risk score by 15%."

- Rule 2: Health Insurance Activity Level: "If daily steps < 3000 for over 60% of the recorded period, then increase health risk score by 10%."

- Rule 3: Heart Rate Variability and Stress: "If heart rate variability < 40ms for over 70% of the recorded period, classify as 'high stress' and increase health risk score by 20%."

- These rules show how specific behavioral data points can be translated into risk assessment metrics within rule engines.

Enhancing Actuarial Tables with Real-Time Data:

- Use rule engines to update actuarial tables in real time based on the latest behavioral data. This leads to more accurate and current risk assessments.

- Automate the calculation of personalized premiums based on the individual risk profile derived from behavioral patterns.

Case Studies

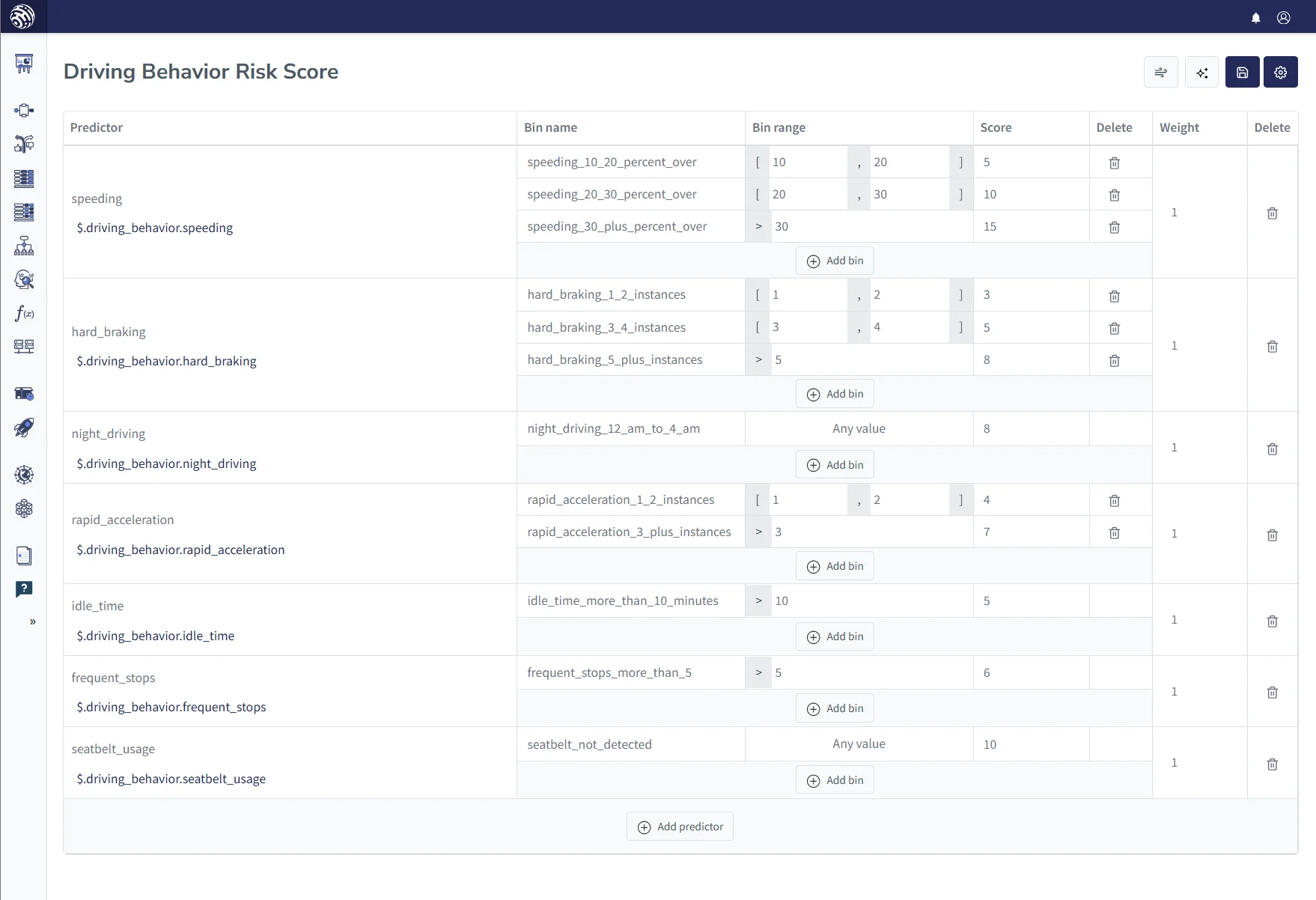

Auto Insurance: Telematics and Risk Assessment

This case study shows how a rule engine with a scorecard system processes and evaluates data from telematics devices to adjust insurance premiums based on driving behavior:

- Telematics Data Collection: Collect data from telematics devices installed in vehicles, including metrics such as average speed, braking patterns, and duration of driving sessions.

- Scorecard Implementation in Rule Engine: Build a scorecard within the rule engine where each driving behavior is assigned a score based on its risk level. For example:

- "Speeding (driving over the speed limit by 20% or more) = 10 points"

- "Hard Braking (more than three instances in a trip) = 5 points"

- "Night Driving (driving between 12 AM and 4 AM) = 8 points"

- Calculating Risk Profile: The rule engine calculates a total risk score for each driver based on the accumulated points over a specified period.

- Premium Adjustment: Premiums are adjusted according to the risk score. For example, a higher total score that indicates riskier driving behavior results in higher premiums.

- Feedback Loop for Drivers: Drivers receive feedback on their driving habits, along with suggestions for improvement, which encourages safer driving behavior.

This practical use of rule engines and scorecards in auto insurance shows how data-driven methods can produce more accurate and fair premium calculations, while encouraging safer driving habits among policyholders.

Health Insurance: Personalized Premiums with Lifestyle Data

Health insurers use rule engines to adjust policy premiums based on individual lifestyle data. This process includes an initial rule set for knockout criteria, followed by a scorecard evaluation:

- Initial Rule Set with KO Criteria: The decision flow starts with a rule set that checks knockout criteria. For example, "If smoker and BMI > 30, then apply KO for standard rates," which may lead to alternative policy options or different pricing structures.

- Scorecard Analysis for Premium Adjustment: After KO criteria are applied, the rule engine moves to the scorecard. This scorecard evaluates factors such as exercise frequency, smoking status, and BMI, where healthier habits lead to lower scores and possible premium discounts.

- Integrated Decision Flow: Integrating KO rules and the scorecard into the decision-making process ensures a complete assessment of risk factors, aligning policy pricing with individual health profiles.

- Feedback for Healthier Lifestyles: Policyholders receive personalized feedback based on their scorecard results, which encourages healthier lifestyle choices.

This structured approach allows more accurate premium setting and aligns underwriting practices with reinsurance capabilities, helping insurers manage risk over time.

| Lifestyle Factor | Criteria | Points |

|---|---|---|

| Exercise Frequency | Daily Exercise | -5 |

| Exercise 3-4 times a week | -3 | |

| Rarely or Never Exercises | 5 | |

| Smoking | Non-Smoker | -5 |

| Smoker | 10 | |

| Alcohol Consumption | Moderate (up to 2 drinks per day) | 0 |

| Heavy (more than 2 drinks per day) | 5 | |

| Body Mass Index (BMI) | 18.5-24.9 (Normal) | 0 |

| 25 and above (Overweight/Obese) | 5 | |

| Risky Behaviors | Participation in high-risk sports or activities | 10 |

| Stress Level | High Stress (as reported or measured) | 5 |

Future of Insurance Underwriting

As technology advances, the role of AI and machine learning in rule engines will likely become more prominent. That will further improve the accuracy of behavioral pattern analysis in insurance underwriting and support more tailored insurance products.

Conclusion

Combining behavioral pattern recognition with traditional actuarial methods through rule engines marks a clear shift in insurance underwriting. This approach improves risk assessment accuracy and supports more personalized, data-driven insurance policies.